What you can afford

Income, Credit, Assets, Collateral

These four components of your financial situation are reviewed by lenders to determine the loan amount for which you qualify: Income, Credit, Assets, Collateral. To qualify means that all four components are analyzed and that your information in each component is sufficient to meet the requirements for the type and amount of loan you want.

Income

Income

A lender starts with the gross monthly income of all persons signing on the loan; they examine the stability of the income source, and how the income compares with amounts that will be going out for all payments on housing and debt; this is known as your ‘DTI’ or Debt-to-Income ratio.

Stability: Two years of continuous employment in the same position is the standard. If you have changed jobs but are in the same line of work, or have advanced within the same line of work or company, you would also be considered “stable”.

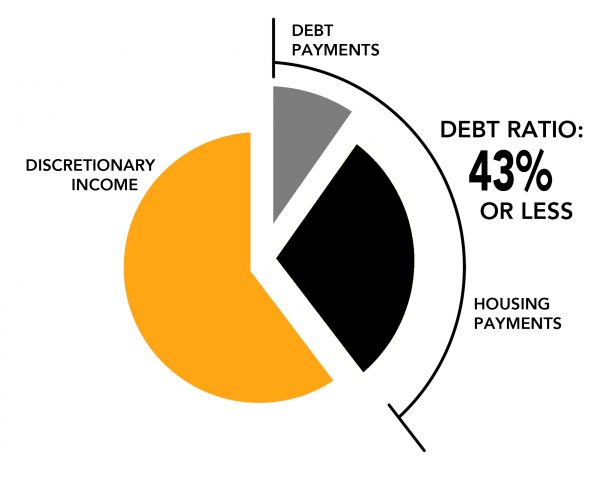

DTI: Your Debt Ratio is often referred to as your DTI (Debt-To-Income ratio). The pie in the chart at right is your total monthly income, and shows the portions spent on debt and housing in gray and black. DTI is calculated as the sum of all payments for both housing and debt expenses, divided by your monthly income, expressed as a ratio (here 43/100, or 43%). As of early 2014, the new “Qualified Mortgage” rules generally require a DTI of 43%.

Credit

A lender will examine a report on your credit drawn from the three nationwide credit bureaus; each bureau presents a score ranging from 400 to 850. With such scores, the higher the better; a score of 680 or higher will generally qualify a borrower for the lowest rates and a score over 720 can provide slightly lower costs on certain programs. If your score is below 680, loans are still available but you will not have as much flexibility in negotiating your loan. If your score is below 620, loans are typically more difficult to obtain and more expensive and may possibly have a higher equity (down payment) requirement. Typical cost for a mortgage credit report today is about $35.

Assets

Assets

A lender will require proof you have enough money for the down payment, closing costs, and fees as they are described in the purchase loan for which you apply. There are programs available for borrowers that do have a lower down payment requirement. In addition, the buyer must have sufficient “reserves” after closing that meet the requirements of the loan program selected.

Collateral

Collateral

The property must provide adequate security for the lender, as verified by an independent appraisal. This means that the property must be in satisfactory condition, that it must be adequate for the intended use, and that the loan amount is limited to a certain percentage of the value of the property (LTV or “loan to value” ratio), as will be defined by the loan program you select.

|

|

Home-buying process

|

| The details can build up quickly, but you’ll have the confidence to deal with each and all when you know the sequence of events you’ll follow.The details can build up quickly, but you’ll have the confidence to deal with each and all when |

|

|

|

First Time Home-buying

|

| If you’re a first-time buyer in the residential home marketplace, you’ve got a lot of new information to tackle. We can help you learn what you need to know, from finding a home to financing its purchase, when it’s relevant to introduce each progressive item.

SPACER |

|

spacer

|

Contact me for more information regarding what you can afford. |

||

|

|

|